Dr. Ngozi Okonjo-Iweala

Dr. Ngozi Okonjo-Iweala

08 June 2013, Abuja – There has recently been a lot of misinformation and misconception in our public debate on debt. My goal in this article is to shed some light on the public debt, to clarify the real state of Nigeria’s debt position, and hopefully, provide a knowledge platform for constructive debate.

Let me say at the outset that no one in government is supportive of a Nigeria that returns to a high state of indebtedness. On a personal note, having gone through tremendous stress during the quest for Paris Club debt relief, I am committed to a Nigerian economy that is fiscally prudent, balances its books and remains at a low state of indebtedness.

To begin, Nigeria’s overall debt is comprised of external and domestic debts. The external debt is typically owed to foreign creditors such as multilateral agencies (for example, the Africa Development Bank, the World Bank, or the Islamic Development Bank), to bilateral sources (such as the China Exim Bank, the French Development Bank or the Japanese Aid Agency), or to private creditors such as investors in our Eurobonds. The domestic debt, however, is contracted within Nigerian borders, usually through bond issues which are then purchased by Nigerian banks, local pension funds, and other domestic and foreign investors. The resources raised typically go to help fund the budget or other domestic expenditures, such as infrastructure projects. We also have some contractor arrears, and other local liabilities which are normally handled through the budget.

Both federal and state governments borrow domestically and externally. However, no state government can borrow externally unless guaranteed by the Federal Government. Similarly, state governments’ domestic borrowing is subject to federal government analysis and confirmation – based on clear criteria and guidelines that a state can repay based on their monthly FAAC allocations and internally generated revenues (IGR).

As a nation, we have had a difficult history with debt. As such, no one can forget the challenging times we went through from 2003 to 2005 trying, in the end, successfully to get relief on our large external debt. Neither the government nor any Nigerian wants a repeat of the country’s past history of large debts. That is why the current President Goodluck Jonathan administration, the Legislature, the Ministry of Finance, and the Debt Management Office, are very focused on a conservative and prudent approach to managing the national debt. Our current approach balances Nigeria’s needs for investment in physical and human infrastructure with a strong policy to limit overall indebtedness in relation to our ability to pay. Above all, any debts incurred must go for directly productive purposes which yield results that Nigerians can see.

First the numbers:

a. In 2004, prior to the Paris Club debt relief, Nigeria’s overall debt stock was very high. External debt stood at US$35.9 billion while the stock of the domestic debt amounted to US$10.3 billion resulting in a total of about US$46.2 billion or 64.3% of GDP excluding contractor and pension arrears.

b. After the successful debt relief initiative, Nigeria’s stock of foreign debt declined dramatically. Indeed, in August 2006, when I left office, Nigeria’s foreign and domestic debts amounted to US$3.5 billion and US$13.8 billion respectively – a total of US$17.3 billion or 11.8% of GDP.

c. By August 2011, when I resumed for the second time as Finance Minister, the domestic debt stock had grown substantially to US$42.23 billion, while the external debt was still a modest US$5.67 billion. This implied a total debt stock of US$47.9 billion or 21% of GDP. Note that while the debt stock grew, our national income also grew so that debt to GDP ratio (the parameter used globally to measure a country’s debt sustainability) remains modest and manageable.

d. Thus, the key noticeable change in Nigeria’s indebtedness in recent years has been the growth of domestic debt. There were two main reasons which resulted in this outcome. First, the initial growth of the domestic debt stock was because the federal government wanted to deepen the domestic debt markets and generate a yield curve for Nigeria which ultimately could help our corporate bodies to access the capital markets and borrow funds at more affordable rates. The DMO through its work has been successful in doing this.

Nigerian corporates can now raise money at reasonable rates at home and abroad, helping them secure resources to invest in the economy. Secondly, however, domestic debt was also raised to finance increased budget expenditures including consumption. For example, in 2010, the 53% salary increase for civil servants was financed by raising domestic bonds. Borrowing for recurrent expenditure or consumption, as was the case here is a practice that is less than ideal and one that we should endeavour not to repeat. We must learn that domestic debt should be incurred sparingly at modest and manageable rates so that government is able to service it and pay back domestic creditors. Failure to do so would severely undermine the finances of our private and institutional creditors to the detriment of the economy.

It is with this background in mind that we have put in place several measures to limit and manage the national debt. There are a number of specific policies we have introduced in the current administration to slow down the increase in our overall debt stock.

a. First, we have brought expenditures and revenues much more in line, through a low fiscal deficit of 1.81% GDP, to reduce the need for domestic borrowing. For example, we reduced annual domestic borrowing from N852 billion in 2011, to N744 billion in 2012, and to N577 billion in 2013. Our objective is to reduce government’s domestic borrowing to below N500 billion in the 2014 budget.

b. Second, for the first time, we have paid down part of our domestic debt rather than rolling all of it over. Beginning in February 2013, we successfully retired N75 billion worth of maturing domestic bonds. And we will continue with this practice in the coming years.

c. Third, we have established a sinking fund with an initial capitalisation of N25 billion. This fund will enable the government to retire maturing bond obligations in the future.

d. Fourth, we are working increasingly with states to get a clearer picture of domestic debts acquired by state governments, thanks to the comprehensive review recently completed by the DMO. Our particular concern is that state governments limit borrowings in line with their incomes and put any borrowings made to work on specific projects and programmes that bring direct beneficial results to their citizens.

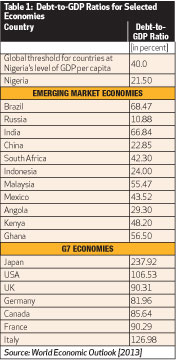

The Debt-to-GDP ratio of selected economies

The Debt-to-GDP ratio of selected economies

e. Fifth, instead of the previous practice of contracting foreign loans in an ad hoc manner, we have streamlined the process for federal and state governments and made it transparent through the Medium Term Rolling External Borrowing Plan, which is reviewed and approved by the National Assembly. This plan presents the anticipated loans to be contracted by the government over a three-year time window, so that we can target funds to priority projects, and also make trade-offs where necessary. Notice that this covers planned foreign borrowing by both the federal and state governments for projects that will yield results in infrastructure, education, health, etc. Most loans contracted are on concessional or very favourable terms. For example, many of the multilateral loans are at zero interests, 40-year maturity, and 10 years grace. Others are at less than three per cent rate of interest.

f. And finally, we have put forward a Medium-Term Debt Strategy with a mix of limited external and domestic borrowing that is appropriate for the economy.

But let me repeat that we shall never be complacent about our national debt. We need to be constantly vigilant to limit the amount of debt and create room for the private sector instead to borrow. As such, we need to stay focused on three main priorities.

First, we should continue to monitor our external borrowing and ensure that we do not slip back to our high indebtedness prior to the debt relief programme. As I mentioned earlier, the External Borrowing Plan, helps to address this concern by ensuring that we always have a comprehensive, transparent view of our foreign borrowing. As at now, our external indebtedness is low at $6.67 billion or about three per cent of GDP.

Second, we should closely continue to monitor and limit our domestic debt, and ensure that it stays within a prudent and conservative range. We should pay off debt that is due to the extent of our ability.

And third, we should also continue to closely monitor borrowing by states to ensure that the debt burdens of our state governments remain within manageable levels and that borrowings are applied to specific projects that yield results for citizens of the state. In that regard, we enjoin banks and other lenders to be careful and prudent when lending to ensure that this is done within the existing rules, regulations and guidelines.

Former UN Secretary-General Kofi Annan once said: “Information and knowledge are central to democracy – and they are the conditions for development.” That is precisely why I have gone to some length to throw light on the real facts and the real issues regarding our debt situation and what the federal government is doing to address them. We need to create the basis to have a healthy and constructive public conversation on this issue, not a distorted and partisan battle.

*Dr. Okonjo-Iweala is Nigeria’s Coordinating Minister for the Economy and Minister of Finance.