– Recession risk rises

– Recession risk rises

Lagos — The US–Israel–Iran war is severely disrupting global energy and logistics markets, heightening recession and inflation risks. With the Strait of Hormuz heavily constrained and commercial shipping facing elevated threats, markets are extremely sensitive to supply losses, delays, and shifting geopolitical risk premiums.

Oil and refined product prices remain volatile, while LNG, freight rates, and war-risk insurance are rising across major trade routes. These pressures increase the likelihood of renewed inflation and weaker growth in the Middle East and beyond, according to GlobalData, a leading intelligence and productivity platform.

The conflict’s operational scope is expanding beyond military targets, increasingly disrupting commercial infrastructure and trade. Ongoing threats to tankers and ports, plus periodic Gulf airspace restrictions, are altering shipping and aviation routes. These disruptions are constraining energy and container flows, lengthening delivery times, and increasing input costs across supply chains.

Ramnivas Mundada, Director of Economic Research and Companies at GlobalData, comments: “The first-order macro shock remains supply-led: energy availability, shipping capacity, and risk premia. Even if oil prices stabilize, the persistence of higher freight costs, longer shipping routes, and insurance costs can keep delivered prices elevated for fuel and intermediate goods. That combination increases the likelihood that inflation proves stickier than expected, complicating monetary policy while weakening real incomes and consumption.”

Conflict-driven cost shocks hit advanced and emerging economies

War-risk insurance premiums for vessels and cargo—as well as aviation insurance and reinsurance—remain elevated, raising the delivered cost of energy and container trade. Higher premiums can render some voyages uneconomic, reduce effective shipping capacity, and accelerate rerouting, further tightening logistics. GlobalData also highlights that financial-market volatility can tighten credit availability, particularly for emerging markets with large external financing needs and high fuel import dependence.

In advanced economies, the key risk is that an energy-and-shipping-driven inflation impulse delays disinflation and complicates the pace of monetary easing. In emerging markets, especially energy importers, the combination of higher import bills and weaker currencies can generate a second-round inflation shock through imported goods and food distribution, while increasing fiscal strain where subsidies absorb part of the shock.

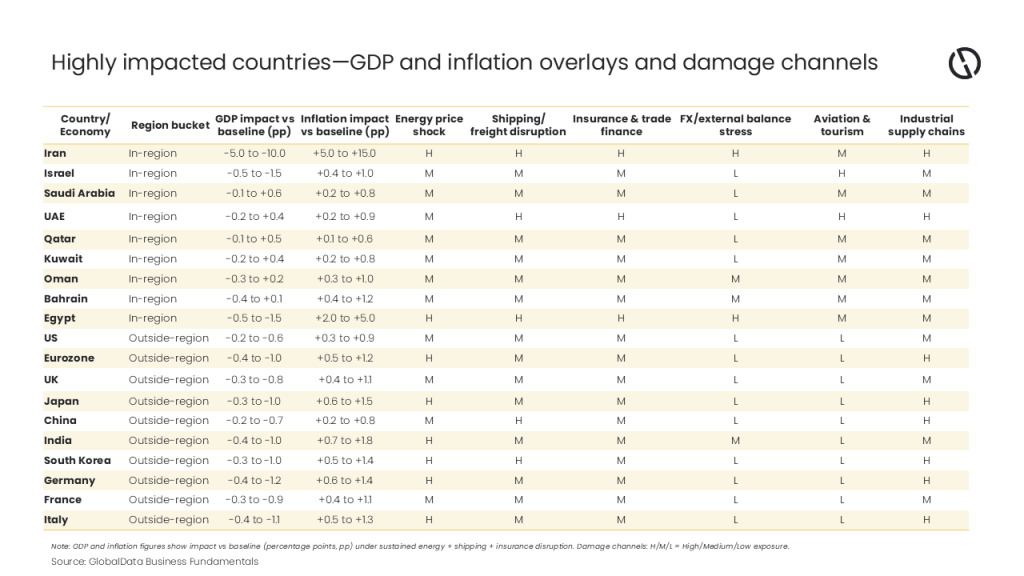

Highly impacted countries: growth and inflation overlays (next 12 months)

Exposure differs sharply by energy balance, supply-chain integration, and sensitivity to shipping and tourism. Hydrocarbon exporters in the Gulf can see partial offsets through higher hydrocarbon receipts, but remain vulnerable to security costs, disruption to trade and aviation, and softer regional tourism. Energy importers in the Middle East and Asia face more direct deterioration in trade balances and higher pass-through inflation.

Where the risk is acute

Iran and Israel remain at the epicenter of downside growth risk. Iran faces the most severe contraction risk under sustained disruption and infrastructure stress, with heightened exposure across energy logistics, insurance and financing channels. Israel continues to face a confidence-led slowdown via weaker investment and tourism, alongside higher defense-related spending that can crowd out private activity.

Energy importers face the sharpest inflation pass-through. Egypt stands out for imported inflation and FX pressures, with fiscal strain likely to rise where subsidies buffer fuel and food costs. In Asia, India, Japan, and South Korea are exposed via higher energy bills and persistent pass-through into transport-heavy components of inflation, raising the risk that headline relief proves temporary.

The Gulf’s offsets are real, but non-oil fragilities are rising. Saudi Arabia, the UAE, Qatar, Kuwait, Oman and Bahrain can see partial macro offsets from hydrocarbon receipts. However, hub economies, especially the UAE, are more exposed to aviation restrictions, shipping/insurance costs and sentiment-driven effects on tourism, trade and services.

Europe’s risk is margin compression and delayed easing. Higher import costs and shipping-linked delivered inflation squeeze industrial profitability, particularly in energy-intensive sectors, increasing the probability that monetary easing is delayed if inflation re-accelerates.

Stagflation risk rises if disruption persists

GlobalData’s base case remains that the longer the disruption persists, the more likely the shock will propagate from headline inflation into broader pricing and activity. If elevated shipping and energy constraints continue beyond a few months, the probability of a global growth downshift increases—particularly for economies already operating with tight real incomes and fragile demand. Under that scenario, the balance of risks shifts toward stagflation-like outcomes: weaker growth alongside inflation that falls more slowly than expected.

Mundada concludes: “While energy and logistics constraints persist, the balance of risks remain titled to the downside. Under sustained disruption and infrastructure stress, Iran’s near-term output risk remains extreme. In Israel, the growth outlook continues to face downside pressure as investment and tourism absorb the confidence shock. For major energy importers, including India, Japan, and South Korea, the risk is a prolonged deterioration in trade balances alongside stickier inflation, especially beyond a few months.”