Lagos — North America will continue to dominate the global liquefied natural gas (LNG) liquefaction capacity additions, contributing about 60% of the total capacity additions between 2023 and 2027, according to GlobalData, a leading data and analytics company.

GlobalData’s latest report, ‘LNG Liquefaction Terminals Capacity and Capital Expenditure (CapEx) Forecast by Region, Key Countries, Companies and Projects (New Build, Expansion, Planned and Announced), 2023-2027’, reveals that North America is expected to witness the highest capacity additions globally, by gaining a total capacity of 284.1 mtpa (million tonnes per annum) from new build and expansion projects during the outlook period.

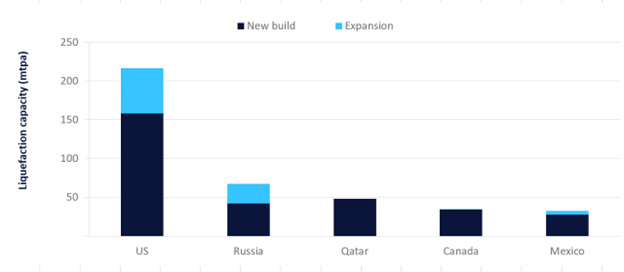

Himani Pant Pandey, Oil & Gas Analyst at GlobalData, comments: “The US will primarily drive the LNG liquefaction additions in North America through 2027, accounting for nearly 76% of the region’s total capacity additions by 2027. Strong global demand for LNG and the availability of abundant shale gas are driving the growth of LNG terminals in North America.”

GlobalData identifies Canada as the second highest contributor to North America’s LNG liquefaction capacity additions, accounting for about 12.3% of the total capacity additions in the region by 2027. The proposed LNG Canada and Bear Head liquefaction terminals are the main drivers for LNG liquefaction capacity additions in the country, with capacities of 14.0 mtpa and 12.0 mtpa by 2027, respectively.

Pandey concludes: “Mexico closely follows Canada, contributing about 11.5% of total LNG liquefaction capacity additions in North America during the outlook period. The Sonora and Amigo floating liquefaction terminals, both being planned in the Sonora state, with 14.1 mtpa and 7.8 mtpa by 2027, respectively, will be the primary drivers of capacity additions in the country.”