Chijioke K. Mama22 December 2014, Sweetcrude, Lagos – The September 1 issue of Time magazine had Republican Congressman Paul Ryan questioned by Time’s Belinda Luscombe in 10 Questions. On a question about Pope Francis calling capitalism “an economy of exclusion” Senator Ryan replied with a candid statement (Ryan is a catholic) He explained that the pope was trying to prevent a system where “you have open markets with no barriers to entry.

In most capitalist economies of the world, government and its agencies frequently make policies that create conditions which works more like “open markets with fully closed doors”. Enter the petroleum industry in Nigeria (Contributing 14.40% of GDP and 75% of government revenues in the rebased GDP figures). Successive Nigerian governments – even the military regimes – have pursued the idea of growing the participation of indigenous Oil and Gas companies in that industry. This is conspicuous in the upstream segment which historically, is an exclusive boutique that sold only to International Oil Companies (IOCs) and foreign Exploration and Production (E & P) companies. The government has implemented a handful of very commendable initiatives to increase the role of indigenous companies. Notably the Local Content Initiative and The Nigerian Marginal Oil fields award rounds.

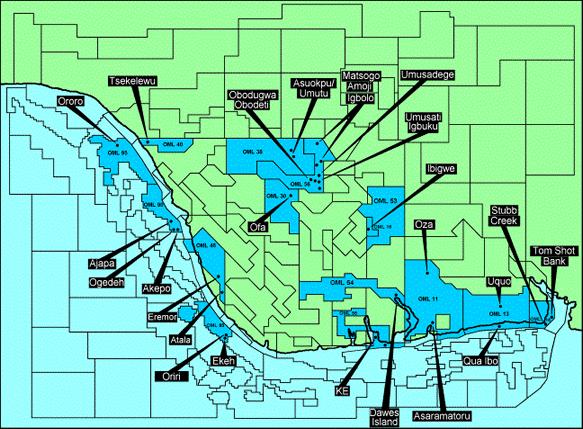

Marginal Oil Fields

Some Nigerian E and P companies have made very laudable progress in the upstream segment. Mention Seplat, Oando, Conoil and some winners of the marginal fields bid round of 2003; Walltersmith, Energia, Niger Delta Resources among others. But a larger number has failed. In 2003, the Nigerian government – in the spirit of opening the market for indigenous upstream companies – awarded (farmed-out) 24 marginal field operating licenses, in a program supervised by its Department of Petroleum Resources (DPR). However, about 65 percent of those fields are yet to be developed or reach first oil – 11 years after. There are a plethora of reasons for this situation – some cogent others flimsy.

These undeveloped fields translate to hundreds (if not thousands) of jobs tied down, in a nations with one of the worst rates of unemployment (an estimated 5.3 million jobless youths). This also means foreign exchange earnings lost (Oil and Gas makes up more than 90 percent of exports in Nigeria) and both government and corporate revenues forgone. Sadly, these are the very advantages that the Petroleum (Amendment) Decree No.23, 1966 sought to derive. (An amendment to the petroleum Act, Laws of the Federation of Nigeria 1990, that introduced Section 16A (3) (a) which provided for Marginal Fields).

By retrieving marginal fields from the original concession owners in their respective OML and delivering it to indigenous firms (through a structured bid process??). The procedure is largely designed to favour Nigerian firms. A former Special Adviser to the Nigerian president on petroleum matters, Dr. Emmanuel Egbogah, and Co-Founder of one of the successful E and P companies in Nigeria, defined marginal fields as “any oil discovery whose production would, for whatever reasons, fail to match the desired or established rates-of-return of the leaseholder” The Nigerian Association of Petroleum Explorationist (NAPE) defines marginal fields as, “non-producing fields whose economics is not considered robust enough using conventional development methods under the prevailing fiscal regime”.

Given the recent strategic actions of most IOCs in Nigeria with respect to portfolio divestment and considering that a vast majority of the over 870 oil fields discovered in Nigeria has not been developed (about 120 are), experts in this industry believe that marginal fields hold the future of Nigerian’s crude oil production. Some have estimated the reserves held in Nigerian’s marginal field to be about 1.3 billion barrels.

At a recent industry event, Nigeria’s Petroleum Minister Diezani Madueke (now also OPEC’s President) opined that the government’s vision for her industry is to increase crude production to 4 million barrels per day (bbl/d) and oil reserves to 40 billion barrels. (The actualization date for this same vision has been shifted many times by previous governments).

While this vision is realizable, the requisite framework maybe absent.

This perhaps accounts for the continued failure in attaining these goals among other problems. Presently, major IOCs (particularly, Royal Dutch Shell and America’s Chevron) are divesting some of their portfolios from onshore and continental shore assets in Nigeria. Shell recently sold OML 18, 24, and 29 to Mart Resources, Pan Ocean, and cash loaded Aiteo/Taleveras consortium respectively.

The current focus for this Big Budget companies is deep offshore. This reiterates the common notion that marginal fields are strategic to the future of petroleum production in Nigeria. Furthermore, the elephant fields discovered in the past decades are gradually turning into brown fields and barrels are declining too, while the much delayed Petroleum Industry Bill (PIB) has made the situation even gloomier by stalling reasonable exploration activities that could lead to big finds. Thus, more and more of already established reserves are coming into the hands of Nigerian firms. But you just asked what they will do with it?

Open Fields

Yes! The upstream business in Nigeria is open to indigenous firms and holds reasonable attraction for foreign investors too. This is demonstrated by some government policies and other trends in the industry already mentioned. Through the marginal fields bid rounds that kicked off in 2013 (currently put on hold) DPR plans to yet award 31 fields. As a mandatory – encouraging – requirement, biding firms or consortiums must (as a minimum) demonstrate an equity structure of 51:49 in favor of a Nigerian entity (individual or corporate) against foreign entities. Favorable petroleum profit tax and incentives exist for winners too. (Although tax giant Deloitte Nigeria pointed out in a recent report that, slight confusion exist in some aspects of royalties and taxes) Indigenous companies that lack the requisite technical competence are also allowed to co-bid or partner with foreign firms (pre or post award). Diverse partnership models are allowed to augment anticipated gaps in local technical skills. Canadian firms (notably Mart Resources Inc. among others) have played prominent roles in this respect in the past. Elsewhere, other firms with deep experience in the application of the unconventional skills, required to recover oil in tight operational conditions are hoping to enter this seemingly open market.

Closed Gates

In this open market, however, the doors are not really open. The very necessary conditions required to ensure a high percentage of success for the farmees are grossly lacking. Industry analysts have continuously canvassed for the creation of more support structures. Government literally delivers these babies without providing a good post-delivery nurse. When analyzed from an enterprise perspective, the statutory role of DPR has little or no contribution to make towards the successful (post-acquisition) development/operation of these fields. Acquirers are left to fend for themselves (especially financially) without the requisite institutional support and fiscal policy. (Acquiring a marginal field cost millions of dollars, from initial application fees to legal fees, signature bonus and royalties) Developing and operating these fields cost yet astronomical amounts of dollars. The farmees often rely on private financial institutions to secure the needed funds. In the 2003 farm-out exercise, a number of Nigerian banks came to the rescue of farmees. Deals were structured! Some went bad! Yet others went very bad! A significant number of the acquirers in 2003 are helpless due to lack of funds (then and more so now).

The credit market in Nigerian may be gloomy for small indigenous E & P firms. The risk of lending to an industry, under the Petroleum Industry Bill (PIB) umbrella of confusion is particularly risky. Consequently, Nigerian Banks may not be very willing to lend because, the last marginal field bid round wasn’t the best lending party. Importantly, local banks are still nursing the wounds of lending to the Electricity Distribution Companies; (DISCOs) loans that aren’t quite performing fabulously according to some experts. The DISCOs will receive additional 213 billion Naira intervention fund (called bailout by some experts) that will somewhat come from commercial banks. Looking offshore for funds is surely an alternative. But foreign financial institutions and investment houses are likely to ask why the home boys are not interested in the soup.

In the too-common Nigerian haste to sell and to buy, marginal field acquirers form organizational structures that are predisposed to cracks, management bickering and ultimate failure. Buyouts and deal restructuring are executed in post-acquisition phase to the detriment of moving on. Local firms engage legal skills that are not competent or sufficiently experienced for the complexity of issues encountered in Farm-Out Agreements (FA). Most frequently, as pointed out by a notable Nigerian Oil and Gas analyst, Dr. Nwaozuzu, acquirers may lack the entrepreneurial drive and rigorous mind required to pursue asset development. Closed doors? Yes! But the keys are available.

The Keys & The Unlocking Strategies

For Nigeria to achieve 4 million barrels per day/40 billion barrels reserve, create jobs, transfer skills to local players and increase revenue (through petroleum resource), marginal oil fields has to produce and optimally too. In the usual optimism of a cock’s flight (that certainly leads to crash-landing) Nigeria sometimes execute elephant project and Einstein-quality ideas with little attention to detail. As the Petroleum Industry Bill is mulled in the legislative house, the features of that bill which would have provided a soft landing for the crash-landing cock (when the flight fails) is conspicuously missing. If status quo remains the same, the forthcoming award round (like the previous one) may not achieve significant success. The current fall in crude prices (although temporal) is a signal to the possible shocks that small volume producers may encounter periodically.

While it is understandable that government is no longer interested in being a business man; there are multiple fiscal policies and conditions that can be created to enable the acquirers succeed and government to attain the national and macro-economic objectives that necessitated the initiative; otherwise the whole aim is defeated. The keys to a successful program do make up a big bunch.

These include a) The establishment of an Energy Bank (with a framework similar to that of Nigeria’s Bank of Industry or The Infrastructure Bank (TIB) but sector specific) to cater for the fiscal needs of the rising number of indigenous E & P firms and other accessorial businesses. The scope and operational frameworks of such a bank will take inputs from multiple areas of expertise.

b) The institution of a high level of transparency in the award process, that ensures the emergence of capable firms with the requisite financial and technical pedigree.

c) The creation of a dedicated and well-structured support program (ideally comprising of a consortium of relevant private sector bodies and concerned public institutions) to provide close, ongoing support (not monitoring) to the E & P firms; in a systematic and structured manner that enhances success rate. This support structure will encompass research-identified, problematic dimensions of marginal field acquisition and operation in the areas of legal, finance/tax as well as, technical challenges.

These and multiple other operator specific-solutions and recommendation, identified/conceptualized through research are the keys to a successful acquisition and operation program.

*Chijioke Mama is a consultant with an indigenous Oil Service Firm and also a marginal oil field researcher based in Lagos, Nigeria. Contact 0706-101-3333 or chijioke.mama@yahoo.com