London — China is the world’s biggest market for crude, importing around 9.7 million barrels a day in the year up to June. In the first half of 2018, before the dispute, China was the biggest importer of U.S. crude, averaging 377,000 barrels per day.

London — China is the world’s biggest market for crude, importing around 9.7 million barrels a day in the year up to June. In the first half of 2018, before the dispute, China was the biggest importer of U.S. crude, averaging 377,000 barrels per day.

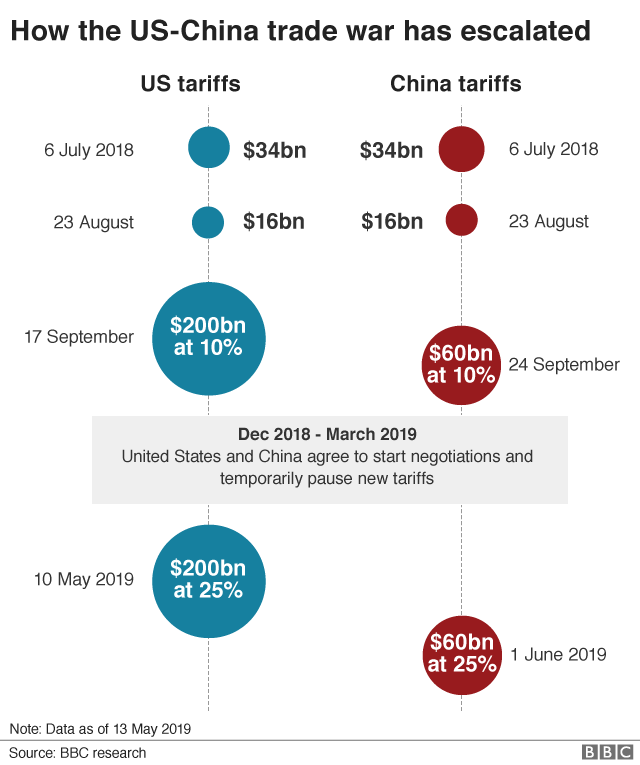

In February this year U.S. crude exports had dropped to just 41,600 barrels per day. On Sept. 1, Beijing imposed a 5 percent tariff on U.S. crude oil imports.

The decline in U.S. oil and LNG exports to China could now get worse. Here, we look at the impact of the current trade war on the American oil and gas industry and after its resolution.

The impact on US crude exports

Although American exporters have diverted some crude towards India and South Korea, this has not made up for the loss of exports to China. U.S. shale oil and gas exploration and production companies have been hard pressed from increases in output which reached 12.4 million barrels a day in September and depressed crude prices.

For example, West Texas Intermediate crude was around $75 a barrel a year ago, but was just $55.47 on Sept. 27, 2019. In the Permian Basin, burgeoning output to 4.5 mbd has been exacerbated by increased production of sweet oil, for which it is hard to find a ready market amongst domestic refineries that are designed to process heavier sour blends of crude. In response, U.S. energy companies have reduced spending on new drilling and completions. The U.S. rig count is now 860, the lowest since February 2018.

American LNG problems

After Japan, China is the world’s second largest market for LNG. According to the EIA, American LNG accounted for 7 percent of China’s total LNG imports in the first six months of 2018 and China received 33 cargoes for the year.

Also Read: Venezuela’s biggest refinery complex restarts some operations

In comparison, during the first 6 months of 2019, China took just 3 cargoes from the U.S. according to a July report from the New China News Agency. Fortunately, U.S. LNG exporters successfully found markets in Europe, which has taken around 40 percent of U.S. LNG exports this year.

The US-China trade war has created a climate of uncertainty for the ten LNG export processing facilities awaiting approval from the America’s Federal Energy Regulatory Commission.

These multibillion projects need confirmed long-term customers to be commercially viable. China, which is expected to increase its LNG imports by at least 40 percent by 2024, represents a big and rapidly growing market for LNG and the U.S. needs access. However, the current uncertainty is delaying final investment decisions on these projects.

The energy industry is also indirectly paying the price of U.S. tariffs on steel imports. Pipelines are made from steel and tariffs have not only increased the cost of new construction but created uncertainty for new export pipes to Gulf ports.

For example, Plains All American Pipeline LP plans to add a fee for users of its new oil pipeline to help compensate for the increased cost of steel.

This trade war has slowed demand for oil, not only in the world’s fastest growing economy China, but also in Europe and America itself. There are now fears of an upcoming recession which will naturally further depress global demand for oil and gas.

The impact of a deal

A resolution of this trade dispute would change the prevailing sentiment and should therefore be good for the world economy. It is likely that demand and investment, together with prices and profit margins will begin to recover.

However, the real question is whether China will open itself to significant amounts of U.S. oil and gas in the future. The U.S. may have opened Pandora’s Box; time will tell.

*Nicholas Newman is an experienced upstream energy correspondent and expert that writes and provides consultancy services for a range of business and media clients worldwide.

Reach Nicholas at [email protected].

like us facebook