Lagos — The 2015 Paris Climate Agreement, which seeks to limit global increase in temperatures to less than 2°C this century, was signed by 195 countries, 33 of which are African. To achieve this ambitious target, significant carbon emission reductions and energy efficient systems are required. As part of the agreement, countries have set out a range of clean energy and energy efficiency targets (“Nationally Determined Contributions”) to cut emissions. Electricity generation is most commonly the leading contributor to CO2 emissions in most countries, at which the majority of NDC in Africa are targeted at. Massive strides have been made into the installation of renewable energy capacity, driving the decarbonisation of the energy sector. The biggest issue surrounding renewables is the difficulty of storing the electricity at scale and for prolonged time without long distant, inefficient transmission, as well as the irregularity of electricity supply from these technologies. While batteries have certainly helped at a micro-scale, they are not yet cost-effective at macro-scale.

Hydrogen, produced through electrolysis of water, is the perfect solution to the problem. Specifically green and blue hydrogen are suitable for further development in Africa. The development of a green hydrogen economy in Africa has since gathered considerable attention, driven by the continent’s high renewable energy potential and investment coming from developed countries desperately looking for means of decarbonising their own industries. Green hydrogen is best positioned to reduce CO2 emissions in typically “hard-to-abate” sectors such as Industry (e.g., construction and steel manufacturing), centralised energy systems, as well as transportation and mobility. Natural gas will form the basis of hydrogen integration as methanation becomes commercially viable and pipeline infrastructure is upgraded to support hydrogen blends.

The EU has introduced its hydrogen strategy in 2020, proposing a shift to green hydrogen by 2050, mainly services through a steady supply coming from Africa. Africa is expected to become the preferred location for the green hydrogen economy due to its growing penetration in renewable energy, greater land availability, easy access to water sources and port facilities, enabling Africa to position itself as a major hydrogen export hub.

Development Finance Institutions (DFI) are thought to be the primary financiers of green hydrogen projects in Africa, as they have mandates for green investments. Additionally, Export Credit Agencies (ECAs) are expected to become major financial contributors; as well as alternative financing structures such as green bonds and green infrastructure funds.

Development Finance Institutions (DFI) are thought to be the primary financiers of green hydrogen projects in Africa, as they have mandates for green investments. Additionally, Export Credit Agencies (ECAs) are expected to become major financial contributors; as well as alternative financing structures such as green bonds and green infrastructure funds.

Despite Africa’s dire energy need, over-supply of electricity has become a significant challenge, primarily driven by poorly maintained generation, transmission and distribution (T&D) systems. Hydrogen production and storage can be a useful technology to solve this problem. Excess electricity can be used to generate green hydrogen during times of oversupply, and in turn be utilised to generate electricity during an undersupply of electricity. Hydrogen is also a suitable clean resource to help decarbonise numerous other industries including transportation, building heat and industrial sectors.

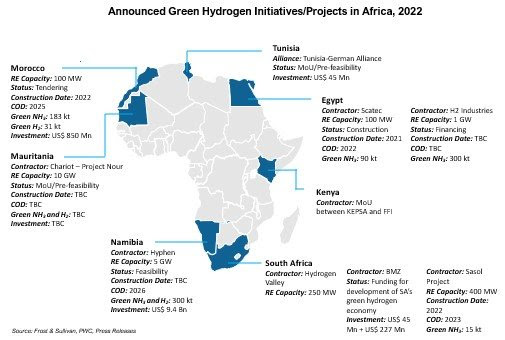

Egypt’s 100 MW Scatec Ammonia plant is the perfect example of how to set up a green hydrogen economy. There are three main steps African countries need to follow in order to seize the green hydrogen opportunity:

1. Installation of a Pilot Plant: Government needs to partner with a private electrolysis company to develop commercial-scale pilot project including a renewable energy plant (Solar/Wind), electrolysis facility and a direct source of demand (i.e., Ammonia plant). This will aid policy makers in developing domestic capabilities, identifying unique local challenges, further developing R&D and crafting initial policies and regulations.

2. Development of Local Policies and Regulations: Once the initial pilot plant has proven commercially viable, government needs to develop comprehensive green hydrogen policy including realistic production targets considering domestic demand and global market trends, defining sector governance and outline policy framework, as well as outline funding structures.

3. Develop an International Export Market: Increased generation and experience with green hydrogen throughout the continent will result in falling production costs in response to economies of scale, R&D development and domestic experience. Export of green hydrogen can be either in the form of liquified green hydrogen to renewable energy deficit countries or in the form of green finished industrial products such as steel, polymers, metals, methanol, etc. A government supported company can be set up to form supply agreements with key export markets which will enable government to build, upgrade or retrofit the required infrastructure for shipping and pipeline channels.

In summary, green or blue hydrogen production is already gathering pace on the continent. While the production is not yet broadly cost competitive as compared to the conventional fuels, it would replace (natural gas, coal). Africa has the opportunity to position itself as a major producer and exporter of green hydrogen as the hydrogen economy in Africa develops, driven by R&D, integration of hydrogen in the value chain and increased capacity of renewable energy in the power mix.

Follow us on twitter